This page covers monopolistic competition in terms of the nature of the market, price and output, profits and losses and efficiency.

Assumptions of the model

A large number of buyers and sellers means each firm has very limited market power.

There are no barriers to entry into or exit from the market.

A market with a large number of producers, each selling a differentiated product.

A differentiated product is where there are slight differences in the products firms in the market sell.

Examples of monopolistic competition

Small shops, hairdressers, plumbers, electricians and care homes are examples of monopolistically competitive markets.

The example used on this page is the hairdressing market.

See page Monopoly 2.11(3) for a numerical example

Demand curve

Each firm in monopolistic competition sells a product that is different to others in the market, they face a downward-sloping demand curve and firms have some control over the price they charge.

Firms in monopolistic competition are price makers.

For example, a hairdresser in a monopolistically competitive market could increase their price and not see the quantity demanded fall to zero because their differentiated product will enable them to retain customers.

Elasticity

There are many competing firms in the market selling differentiated products which means the demand for the good or service of individual firms in the market is price elastic.

Revenue

The demand curve is downward sloping the average revenue and marginal revenue curves are separate, and the marginal revenue is twice as steep as the demand curve and is negative when demand becomes price inelastic.

Costs

The short-run cost curves of the firm in monopolistic competition are affected by the law of diminishing returns as they are in perfect competition. The marginal cost and average cost are U-shaped.

Profit maximisation

Firms aim to profit maximise in monopolistic competition by producing where marginal cost equals marginal revenue when marginal cost is rising. Price is set on consumer demand at this level of output.

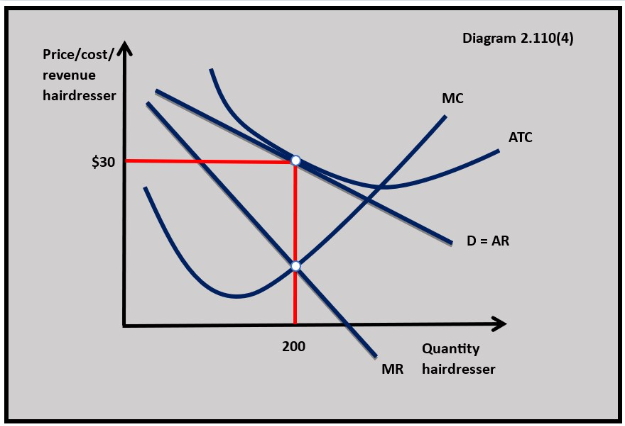

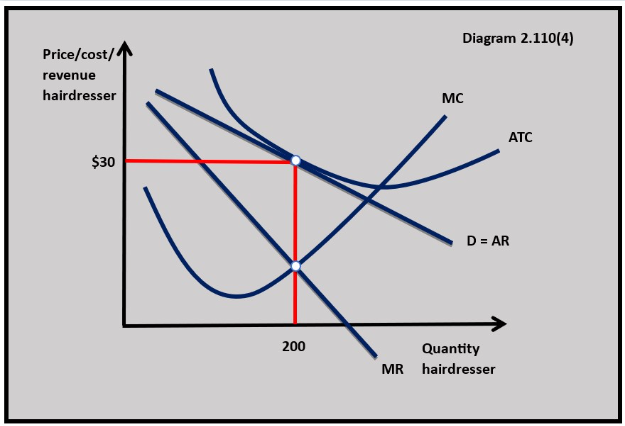

Price, output and profit maximisation are shown in diagram 2.110(3).

Normal profits

Normal profit exists in monopolistic competition when total cost equals total revenue at the profit-maximising output.

In diagram 2.110(4), this will be where average total cost equals average revenue at the profit maximising output:

(AR = ATC) x Q

When firms in the industry are making normal profits, the market is in equilibrium which means entrepreneurs are making enough profit to keep their business in the market.

In the hairdresser example in diagram 2.110(4), the firm is making normal profit at a price of $30 and an output of 200 haircuts.

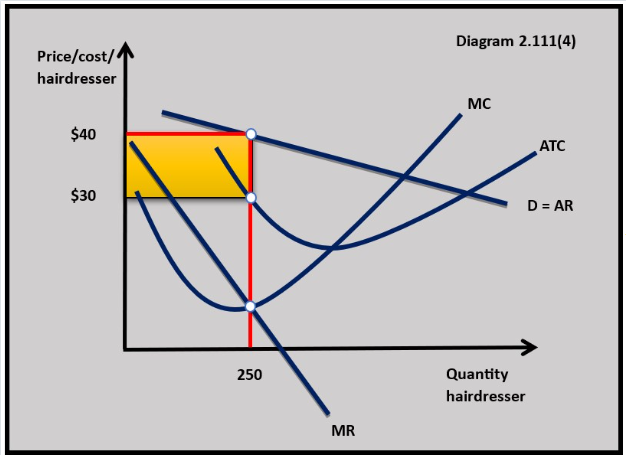

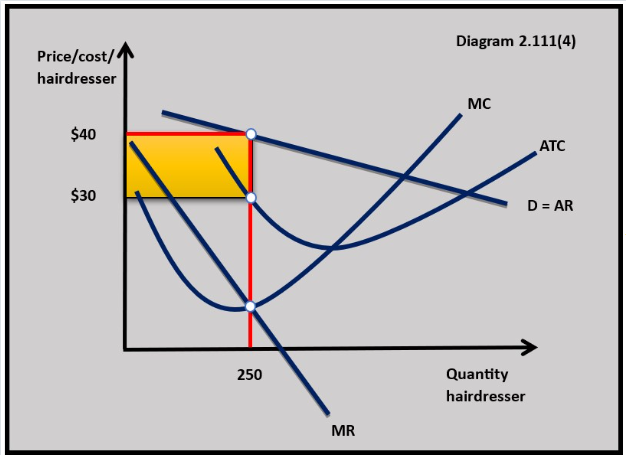

Abnormal profit

Abnormal profit in monopolistic competition is where total revenue is greater than total costs and the firm is making more than the minimum profit required to keep it in the market.

Abnormal profit in monopolistic competition is where total revenue is greater than total costs and the firm is making more than the minimum profit required to keep it in the market.

In diagram 2.111(4) this is where average revenue is greater than the average total cost at the profit-maximising output.

(AR – ATC) x Q = abnormal profit

In the hairdresser example, the abnormal profit is:

($40 - $30) x 250 = $2,500

Abnormal profit is a short-run equilibrium situation.

In the long run, the abnormal profit attracts new firms into the market and the demand curve for existing producers in the market decreases.

New firms stop entering the market when the abnormal profit is competed away and all the firms in the market are earning normal profits.

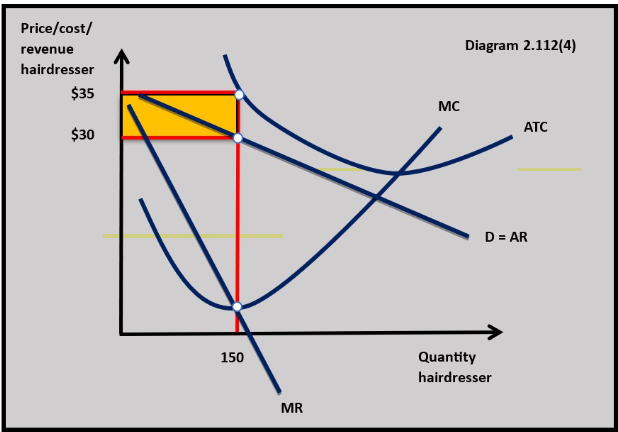

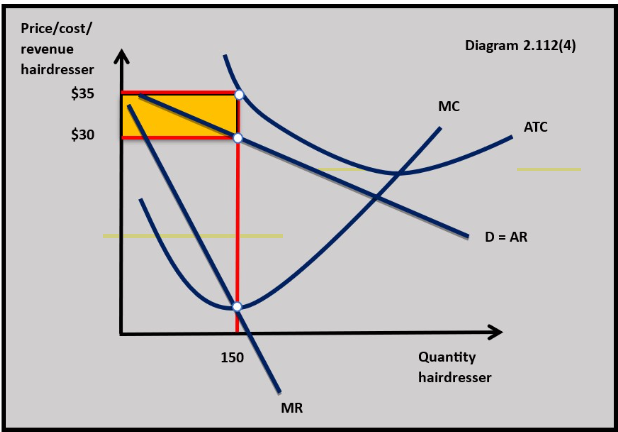

Losses

Losses in monopolistic competition mean total cost is greater than total revenue and firms are not making the minimum profit required to keep producing in the market.

In diagram 2.112(4) this is shown where the average total cost is greater than average revenue.

(ATC – AR) x Q = losses

In the hairdresser example, the loss is:

($35 - $30) x 150 = $750 loss

Losses are a short-run equilibrium situation.

If firms in the market do not earn the minimum profit needed to keep them in the market (normal profit) they will leave the industry.

As firms leave the market there will be less competition for existing producers and this will cause the demand curves for these firms to increase returning the firms to normal profit in the long run.

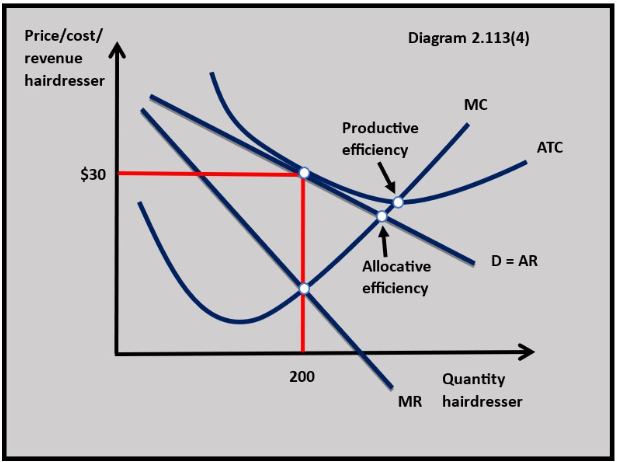

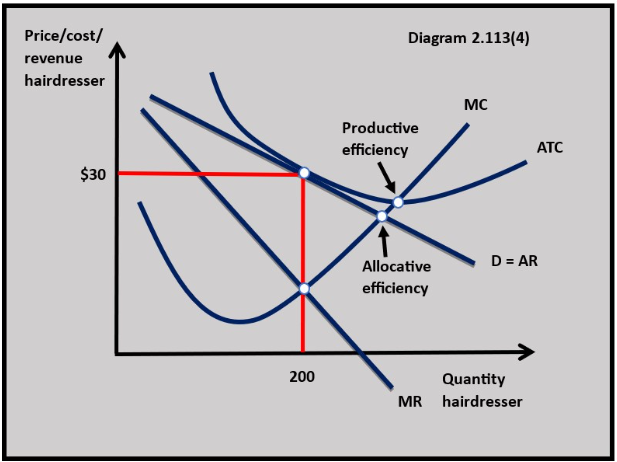

Productive (technical) efficiency

Productive efficiency occurs in monopolistic competition when all firms in the market produce at the minimum average total cost where marginal cost equals average total cost at the profit-maximising output.

Firms in monopolistic competition do not achieve productive efficiency because they do not produce where marginal cost equals average total cost. This is shown in diagram 2.113(4)

Allocative efficie ncy

ncy

Allocative efficiency is achieved when demand equals supply in the market or where firms set price equal to marginal cost and the community/social surplus is maximised.

In monopolistic competition, firms profit maximise by charging a price above marginal cost and producing an output below the allocatively efficient level. This is shown in diagram 2.113(4)

Evaluation of monopolistic competition

Most markets are made up of businesses of different sizes and cost structures. Even where there are many small firms in the market, large firms are likely to exist.

Monopolistic competition is neither allocatively nor productively efficient compared to perfect competition, but it does offer the consumer more choice because firms sell differentiated rather than homogenous products.

a. Explain why firms in monopolistic competition cannot make abnormal profits in the long run. [10]

Twitter

Twitter  Facebook

Facebook  LinkedIn

LinkedIn