This page covers the nature of minimum prices and the reasons why governments use them. It also covers the impact of minimum prices on different stakeholders.

Definition

A minimum price or price floor is a lower limit set by the government or controlling authority to stop the price of a good or service from falling below a certain level.

Reasons for minimum prices

Governments use minimum prices or guaranteed minimum prices to protect producers in markets.

This is often the case in agricultural markets where governments look to support farmers and protect the food supply.

Effects of a minimum price

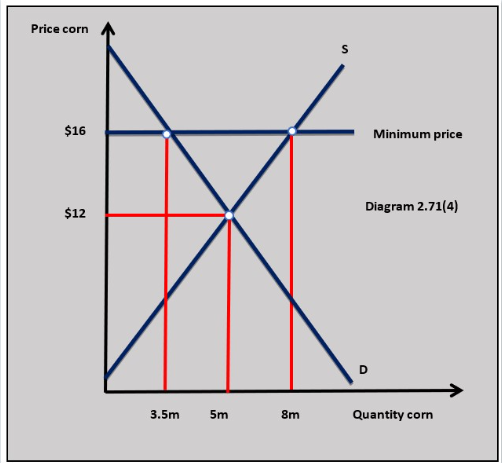

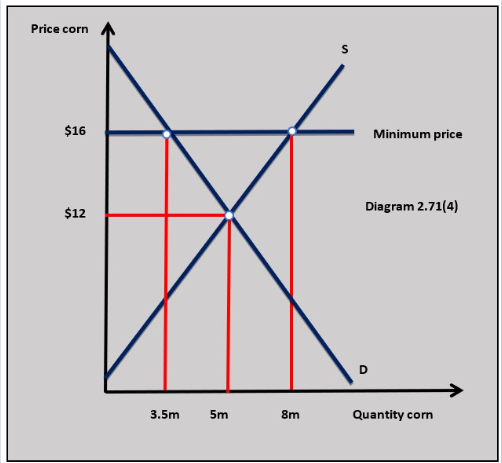

Diagram 2.35 is an example of how minimum prices might work in the market for corn. In this example, the equilibrium price for corn is $12 per bushel with 5 million units of output. A minimum guaranteed price is put in place at $16.

Diagram 2.70(4) illustrates the impact of a minimum price on the marke t for corn.

t for corn.

- As the price rises from $12 to $16, the QD for wheat falls to 3.5 million bushels.

- QS of corn increases to 8.0m bushels because the higher price increases producer profits and covers the costs of higher production.

- At the minimum price, the QS is greater than the QD and there is excess supply or surplus output. In diagram 2.71(4) this is (8.0m – 3.5m = 4.5m units).

- To maintain the minimum price the government needs to purchase the surplus and put it into storage. The cost of the government intervention is 4.5m x $16 = $72m

- The wheat needs to be stored and this is an additional cost of the scheme. This can be particularly expensive for goods that need to be refrigerated.

- Additional agricultural producers are attracted to the market by the minimum price which leads to an increase in excess supply in the long run and reduces supply in other markets.

Consumers

Consumers lose surplus when a minimum price is set above the equilibrium price because they need to pay a higher price for the good.

Consumers lose surplus when a minimum price is set above the equilibrium price because they need to pay a higher price for the good.

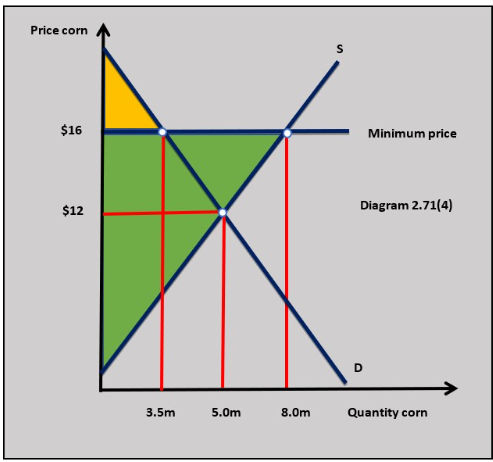

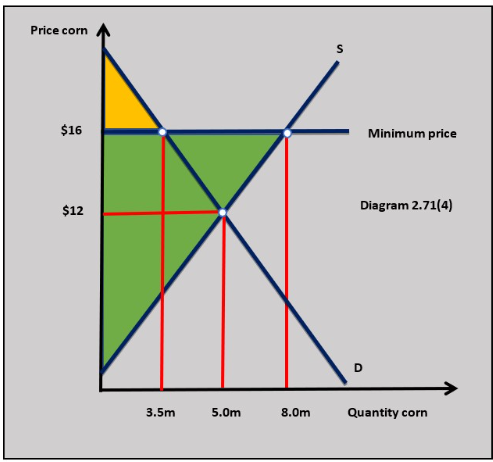

The loss of consumer surplus from the minimum price put on wheat is shown in diagram 2.71(4). The yellow-shaded area shows the new consumer surplus following the increase in price from $12 to $16.

Producers

Producers gain when a guaranteed minimum price is above the equilibrium price because their producer surplus increases.

This means they will receive higher revenues and profits.The increase in producer surplus is shown by the green-shaded area in diagram 2.71(4).

Government

Minimum prices represent an opportunity cost to the government. There is the cost of the government buying the excess supply along with the cost of storing it and managing the system.

Welfare

Minimum prices can lead to a misallocation of resources in agriculture markets, with huge surpluses developing at the expense of reduced production in other markets.

There is the cost of waste when excess supply is destroyed when it cannot be sold.

The gains of a minimum price tended to be concentrated amongst producers, with dispersed losses for consumers and taxpayers.

Explain the implications for different stakeholders on a minimum price in an agricultural market. [10]

Twitter

Twitter  Facebook

Facebook  LinkedIn

LinkedIn