This page covers the introduction to Economics as a subject. It includes Economics as a social science, scarcity, resources, opportunity cost and the production possibility model.

Defining economics

Economics is a social science because it studies human behaviour in relation to the economy.

Economics is a social science because it studies human behaviour in relation to the economy.

Economics is the study of how society allocates scarce resources to satisfy human wants.

Human wants are people’s desire to consume goods and services to derive satisfaction from their consumption.

Resources are the factors of production used to produce goods and services. Resources include:

- Land provides the raw materials used in production.

- Labour are the workers used in the production of goods and services.

- Capital is the machinery and equipment used to produce goods and services.

- An entrepreneur is a person or people who combine and manage the factors of production (land, labour, and capital) to produce goods or services and make a profit.

The economic problem is unlimited human wants are chasing too few resources, which is the central economic problem of scarcity.

Economic goods are products produced using scarce resources.

Free goods arise because some resources in certain situations are not scarce.

The allocation of resources means the distribution of the factors of production to produce different goods and services in an economy.

Sustainable economic activity is the use of scarce resources to produce goods and services in the present that do not impact their availability in the future.

The central economic problem of scarcity forces different economic stakeholders to make choices between alternatives because they cannot have everything they would like to have.

Opportunity cost is the highest value alternative foregone for the option chosen in a decision-making situation.

An economic system is how society is organised and governed, affecting the resource allocation in the economy. The three systems are:

- Free market economies - where the interaction of demand and supply in markets determines the allocation of resources in an economy.

- Planned economies - where the state determines the allocation of resources in an economy.

- Mixed economies - where market forces and the government determine the allocation of resources.

Production Possibility Curves (PPC)

Definition of the PPC

A production possibility curve is a model that shows the maximum relative amounts of two goods a country can produce with a given resource availability at a given point in time.

The PPC model is based on the relative quantities of any two goods that an economy can produce.

The production possibility curve diagram

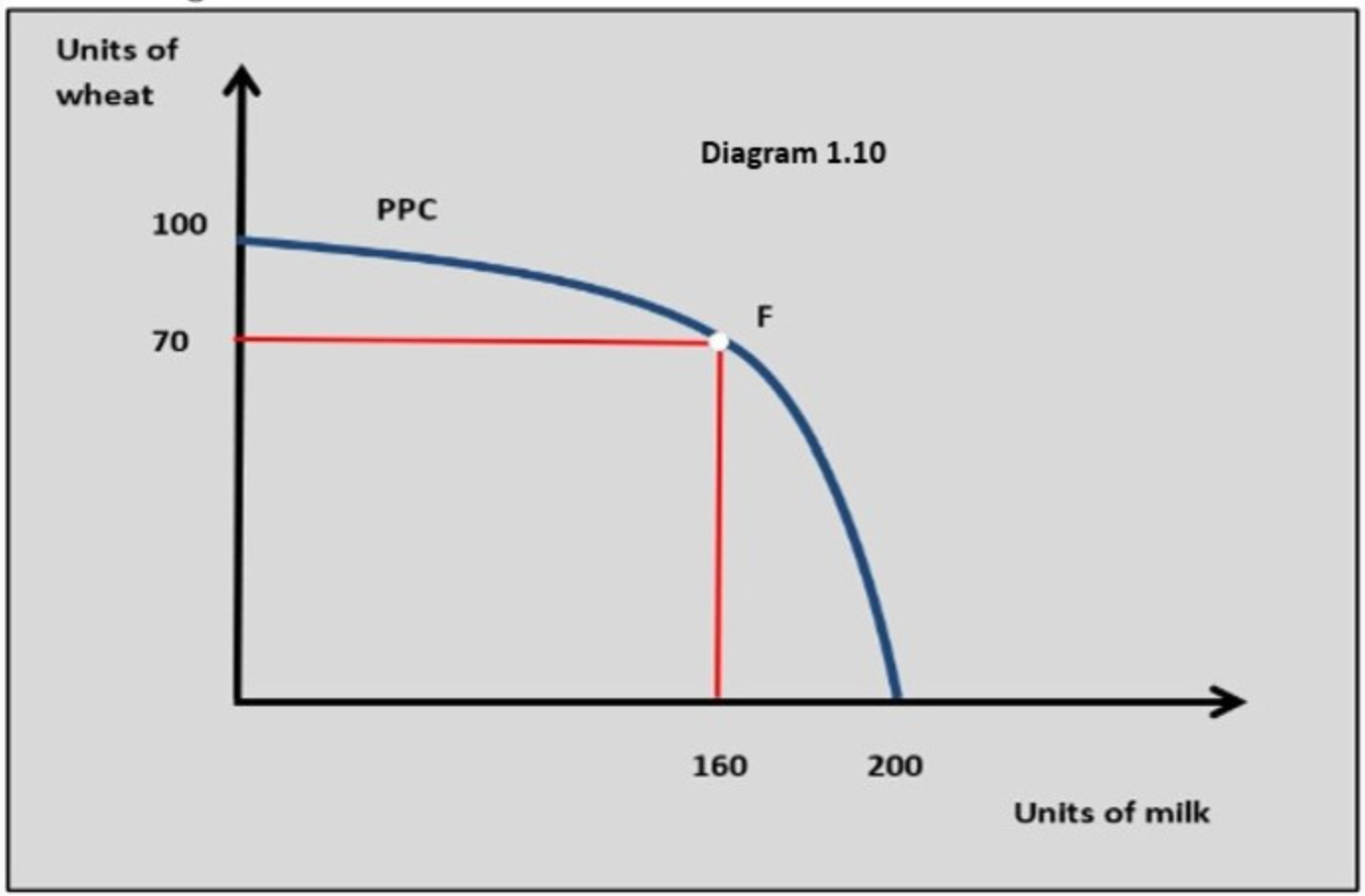

The PPC curve in diagram 1.10 shows the relative quantities of wheat and milk the economy can produce. At point F, the economy produces 160 units of milk and 70 units of wheat.

The PPC curve in diagram 1.10 shows the relative quantities of wheat and milk the economy can produce. At point F, the economy produces 160 units of milk and 70 units of wheat.

The diagram illustrates:

- Scarcity on the PPC curve

- Opportunity cost because producing units of milk (160 units) means foregoing the production of wheat (30 units)

- Increasing opportunity costs as resources move from producing milk to producing wheat.

- Constant-cost PPCs are straight-line PPCs in which the opportunity cost stays the same as resources are moved from producing one good to another.

- All points on the PPC represent the productively efficient output.

- Producing inside the PPC means the economy is not achieving productive efficiency.

Growth in production possibilities

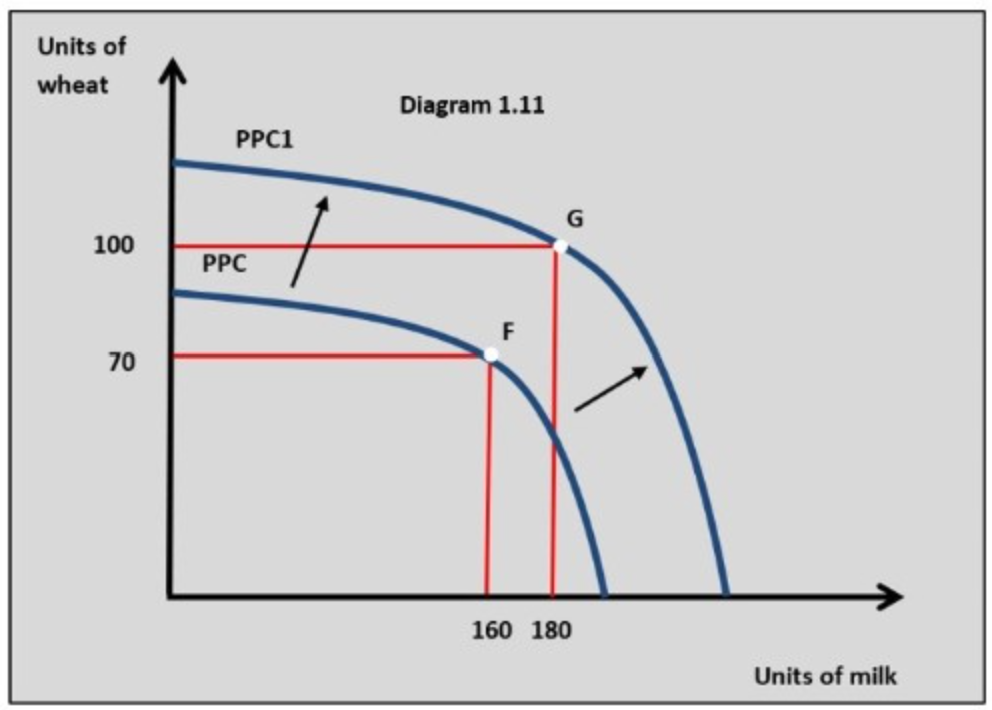

The growth in production possibilities occurs when the potential output of an economy increases over time.

The growth in production possibilities occurs when the potential output of an economy increases over time.

As potential output increases, the PPC shifts outwards, and the economy can produce more milk and wheat.

This is shown in PPC diagram 1.11, where PPC shifts to PPC1, and potential output increases from point F to point G. This means that the economy's potential output increases from 70 units of wheat to 90 units and from 160 to 180 of milk.

Using the production possibility curve model, explain the concepts of scarcity, opportunity cost and the allocation of resources. [10]

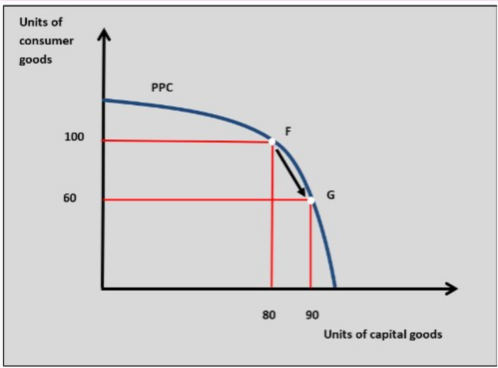

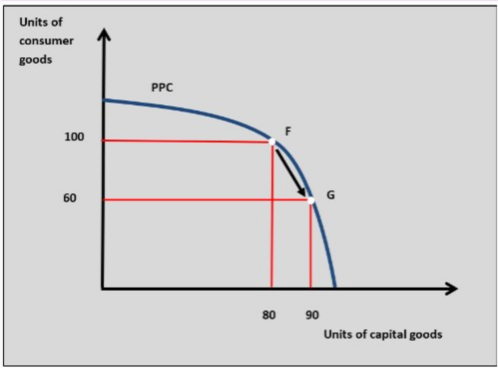

The PPC diagram shows more resources being allocated to the production of capital goods (80 units to 90 units) leads to an opportunity cost in terms of fewer consumer goods being produced (100 units to 60 units).

The PPC diagram shows more resources being allocated to the production of capital goods (80 units to 90 units) leads to an opportunity cost in terms of fewer consumer goods being produced (100 units to 60 units).

Twitter

Twitter  Facebook

Facebook  LinkedIn

LinkedIn